Level up with in-network providers

Table of Contents

Your healthcare network is special. It’s the type of network that doesn't require corporate mixers or LinkedIn requests — your insurance company has already made the connections you need for your healthcare concerns.

When a health care provider is in-network, it means they’ve already come to an agreement with your insurance company to provide services at a set rate. Usually, this rate is significantly cheaper than what you’d pay for the same service without coverage or from an out-of-network provider.

Ready to start your in-network search, wondering what the benefits are, or curious about what will happen if your provider is out-of-network? Here are a few helpful tidbits to keep in mind.

How to search for in-network providers

There’s a big world of in-network providers out there, and navigating that world can be confusing. Where do you start? How do you know if a provider is in-network? What if your favorite provider isn’t in-network? All great questions — and ones that your health insurance company can help you answer.

If your health insurance provider has an online portal, here’s a step-by-step guide to starting your search. Keep in mind that most health insurance providers will typically only display care options that are in-network.

Navigate to your health insurance provider's search portal or directory.

If you can filter results, consider narrowing down your search with criteria like the type of care you’re looking for, distance from your home, and patient reviews.

Try making a list with a few potential options, just in case the medical provider you choose isn’t taking new patients or doesn’t have availability that works for you.

Call the medical providers on your list to see if they are accepting new patients, take your insurance, and have availability (sometimes specialists take months).

With this information in hand, weigh your options and decide who is the best fit for you.

If your health insurance provider doesn’t offer an online search function, then the next best idea is to call them and ask for a list of eligible providers.

Keep in mind that online directories often change or get out-of-date. It’s a good idea to call the health care provider directly and double-check that they’re in your network.

Tips on finding and choosing mental health providers

Your health care provider is probably great, and they may be able to address some of your mental health concerns. Sometimes, though, you may benefit from seeing a more specialized professional.

It can be daunting to start the search for a mental health provider or counselor who understands your unique needs. Luckily, there are plenty of resources that can help find the right fit.

Ask for a referral or recommendation

If you have a primary care provider and feel comfortable sharing with them, they may be able to refer you to a few local mental health specialists. Because your provider likely already knows you and how what you’re going through is affecting your health, they should be able to make more informed suggestions.

Close friends and family members may also be able to provide recommendations. If you don’t have the energy or resources to find a mental health professional and schedule an appointment, they may be able to help you clear those hurdles.

Check for an Employee Assistance Program (EAP)

EAPs are voluntary, confidential programs provided by your employer. Oftentimes, EAPs include resources like mental health services for free or reduced cost. You can likely find a provider through your EAP, or at the very least, get immediate help until you can find something more permanent.

Usually, instructions for how to access your EAP and the details of what’s included can be found in an employee handbook or online portal.

If you don’t have any luck locating either of those on your own, you can always get more information from your employer or HR department. They can provide you with a full list of what’s available, and guidance on how to use the program.

Use online tools to help your search

There are many online portals that can help you find mental health services, including your health insurance provider’s website. Most of these search tools will let you narrow down your options based on factors like location, specialty, gender, and cost.

Keep in mind that some of these tools will charge providers to be listed on their site, so there’s a good chance that not all local options will be listed. You can always do a Google search for “mental health providers near me,” then dig into the results to narrow down your options.

Have questions prepared and written down

At your initial meeting, you can ask your potential mental health professionals a few questions to get a feel for the fit. It can help to prepare these questions and write them down before you get on the phone/in the room.

Often, your first consultation will be free, but it’s a good idea to get some info on their payment structure and plans beforehand. If you haven’t done that yet, now’s the time to ask.

Here are other questions to consider:

What’s your experience in dealing with concerns like mine?

What kind of license and background do you have?

What type of therapy would you recommend for me?

How long and how often would we meet?

Is therapy offered in-person, online, or both?

What does a typical session look like?

How are cancellations handled?

Do you have after-hours availability for emergencies?

How do you evaluate if therapy is effective?

Would you consider prescribing any medication?

Do you observe any Diversity, Equity, and Inclusion best practices?

Choosing the right type of care: Urgent Care vs. ER

Sometimes a medical issue requires immediate attention, and choosing between urgent care versus the ER isn’t a decision to be taken lightly. Understanding the difference between the two options can ensure you get the proper level of treatment and potentially save big on medical bills.

The first step is evaluating your symptoms, the urgency of the situation, and the distance you’ll need to travel for each option. From there, you can make an informed decision on urgent care versus the ER.

Urgent care: Ideal for non-life-threatening conditions

Urgent care centers are perfect for minor illnesses and non-urgent injuries. They can handle things like sprains, fractures, stitches, and the flu, but they’re not equipped to deal with life-threatening situations.

Urgent care centers are usually open in the evenings and on weekends, but most aren’t open 24 hours. Urgent care is also typically more affordable than an ER visit, and wait times are shorter. Some may require an appointment in advance.

Emergency room: Ideal for severe conditions

If you have a severe condition — like difficulty breathing, major injuries, allergic reactions, or any other symptoms that could indicate a serious problem — then you should probably head to the emergency room.

ERs are typically staffed with full-scale medical teams and have advanced resources and technology to diagnose whatever you’re dealing with and set you up with the best possible care plan. If you’re worried about the cost, remember that your health is priceless — and that many hospitals offer payment plans that can help you manage any bills.

If you’re dealing with an emergency situation, you shouldn’t have to worry about whether or not the doctor you see is in-network. Insurance plans usually cannot charge you more for out-of-network providers or penalize you for not searching ahead of time if you’re truly dealing with an emergency.

Urgent care vs. ER

Benefits of finding in-network providers

The main benefit of getting care from in-network providers is saving money — which is a pretty major benefit, if you ask me and my bank account.

1. Reduce your out-of-pocket costs.

When you visit a doctor or healthcare facility in your network, you can typically look forward to lower costs for care — all you have to do is flash your insurance card. Your insurer has already worked out a deal with in-network health care providers, so there aren’t likely to be any major surprises once your bill comes.

2. Most costs can be applied to your out-of-pocket maximum or deductible.

When you see an in-network provider, most expenses you pay are usually applied toward meeting your deductible or out-of-pocket maximum.

You know those big thermometers that people use for fundraising, where they color in the amount they’ve received so far? Your deductible and out-of-pocket maximum are kind of like that, except once the thermometer is fully colored in, your insurance will often start covering most or all of your medical costs.

Not only does shopping in-network save you money upfront with lower costs, but you’ll also be making progress toward filling your thermometer.

3. Costs are usually easier to understand.

Health insurance lingo is its own language — and while I might be fluent in it, a lot of people find it understandably confusing, especially when it comes time to decipher the bill. The beauty of sticking with in-network providers is that the billing process will almost always spell out exactly what you’re paying for.

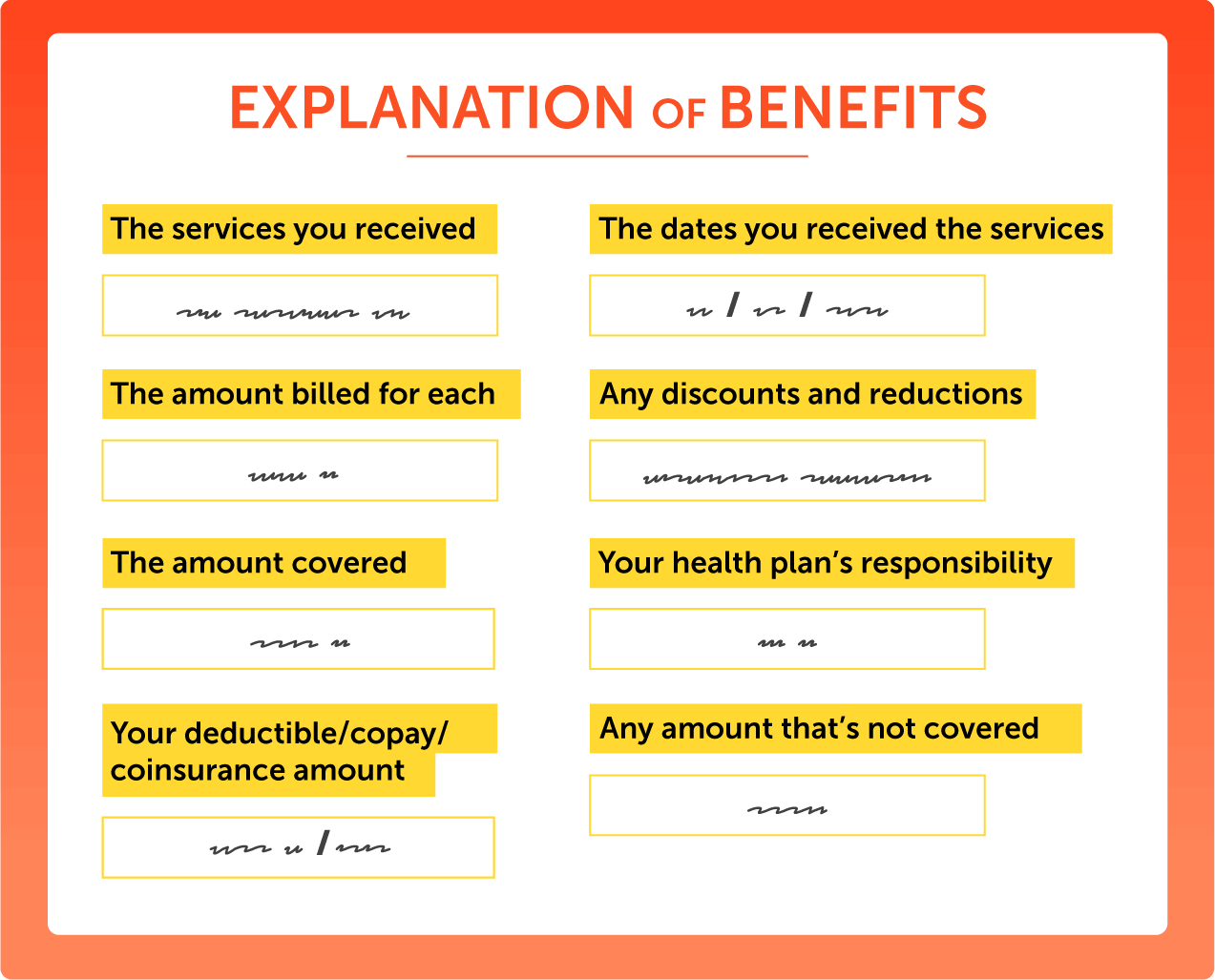

After you visit an in-network provider, your insurer should send you an explanation of benefits. This statement usually outlines a few things.

The explanation of benefits isn’t a bill — you can expect that later from your health care provider — but it gives you a clear understanding of what you’re paying for. If you have any questions about a service that is or isn’t covered, you can always reach out to your insurer.

What to do if your provider isn’t in-network

If your provider isn’t in your insurance network but you still want to continue seeing them, you have a few options. Keep in mind, though, that you may still end up paying much more than you would with an in-network provider.

Check for out-of-network benefits

While it’s true that out-of-network providers are usually pricier, it doesn’t necessarily mean that you won’t have any coverage. A lot of insurance plans offer out-of-network benefits, which means they’ll still contribute toward your medical expenses, just at a lower rate and/or higher deductible.

You can get familiar with your insurance’s out-of-network benefits by checking your online portal or speaking directly with a representative.

Get advice from your health care provider

Your health care provider will likely have your best interests in mind and can help you understand your options. Some may even be willing to grant discounts or special rates for their services, or give you a full rundown of costs before appointments so you understand exactly how much you’ll have to pay.

If you have a preexisting relationship with your provider, they may be able to refer you to an in-network provider that’s compatible with your needs.

Look into network exceptions

In some circumstances, your insurer may be willing to make an exception and treat an out-of-network provider as if they were in-network. Typically, this process is reserved for cases without a suitable in-network provider to address your medical needs.

If you’re granted an exception, then you would pay for care at in-network costs, and payments would go towards your deductible or out-of-pocket maximum.

Keep in mind that getting a network exception is not a guarantee, and you should hold off on seeing your out-of-network provider until you’re approved by your insurer.

Re-evaluate your options during open enrollment

If you find yourself frequently needing out-of-network care, then it might be worth considering switching insurance plans. During your next enrollment period, shop around from the plans available and check their provider networks.

You can only change plans during your open enrollment window or if you go through a qualifying life event (which may include moving states, getting married, or adding a child to your family, for example), so make sure you plan ahead.

ALEX

My network is literally computer servers. Your network is care providers. Here's how to navigate ‘em.